Welcome back to The SaaS Report.

Q2 delivered one of the most interesting mixes of numbers we've seen in a while - from steady deceleration at some of the biggest enterprise names, to surprising re-acceleration in parts of the data infrastructure world, to Marc Benioff’s unexpectedly sober take on the state of GenAI.

In this post, we break down Q2 results from Okta, CrowdStrike, MongoDB, and Snowflake, and then dive into Benioff’s appearance on 20VC, where he offered rare clarity on where AI can actually move the needle - and where the hype is still outrunning reality.

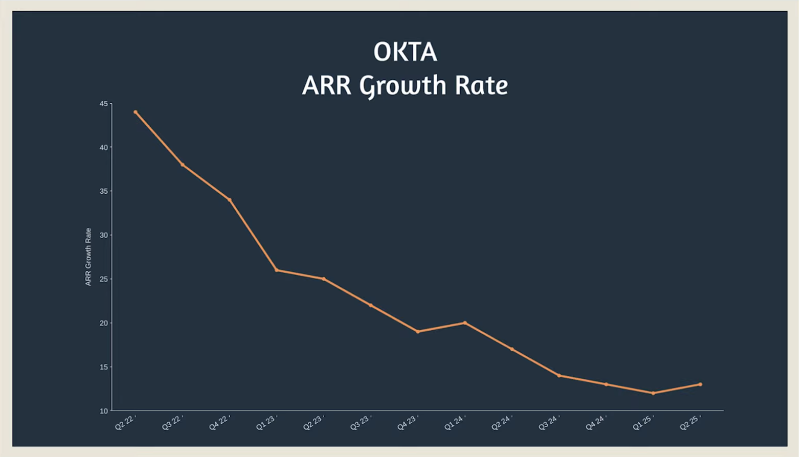

Okta: Slow Growth, Smarter Operations

Okta’s Q2 was a microcosm of the broader SaaS environment:

growth cooling, efficiency improving.

Their ARR grew 13% year over year - good for $316M in net new ARR, but down from $360M a year ago.

A multi-quarter trend of deceleration continued, but the other half of the story is the one investors care about right now:

- FCF margin improved from 8% → 22%

- Operating margin swung from –3% → +6%

- CAC payback tightened from 32 → 24 months

- S&M spend dropped from 37% → 34% of revenue

Net new ARR also grew nicely: $152M this quarter vs. $116M last year.

Rule of 40 came in at 35, Rule of X at 47, and RPO grew 18% to $4.15B.

It’s not a hypergrowth business anymore - but it’s a much healthier one. The market reacted with a modest 3% bump, putting Okta at a 5.7× ARR multiple. In 2021, a business like this might have traded at 15×; in 2025, this is the new reality.

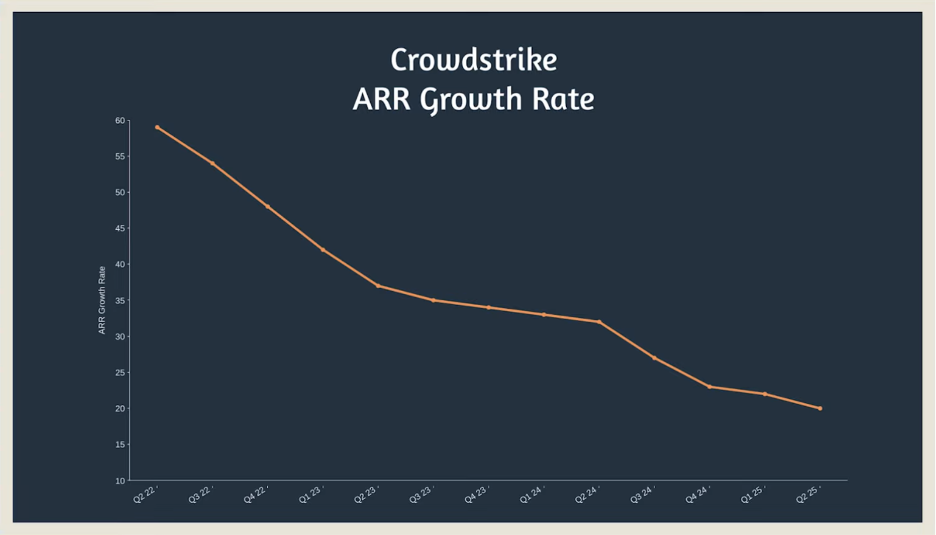

CrowdStrike: A Great Company With an Expensive Price Tag

CrowdStrike added a staggering $739M in net new ARR over the past year.

That’s elite performance.

But the growth rate behind it continues to compress, falling from 54% in 2022 → 20% today. Some of that deceleration is expected - scaling from $500M to $4B ARR is a different sport entirely - but investors now want to see stabilization around the 20% mark.

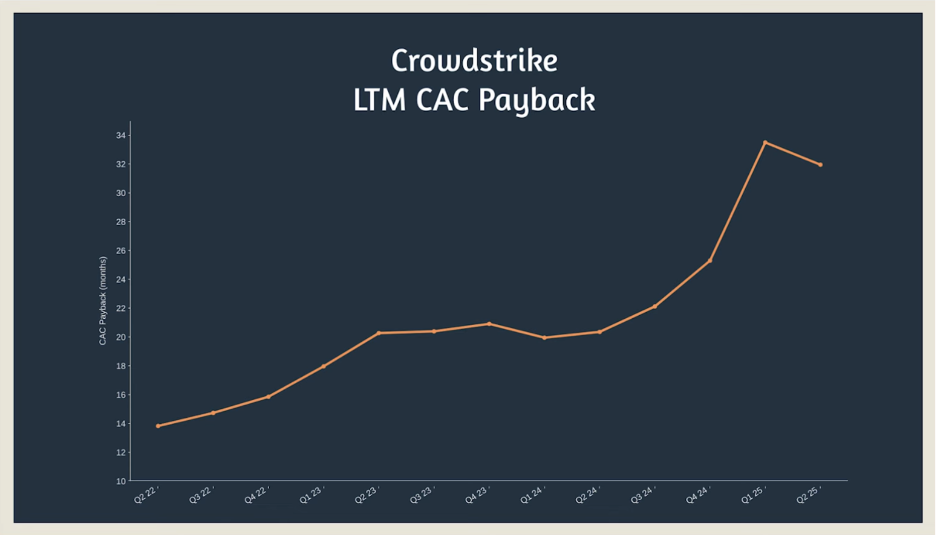

The bigger concern: go-to-market efficiency is slipping.

- CAC payback has more than doubled: 14 → 34 months

- And it’s still trending upward

This isn’t unusual at scale, but the question is whether CrowdStrike can put a floor under it - or whether they drift toward the 40–60 month CAC paybacks we’re seeing from other large enterprise vendors.

The part that doesn’t quite add up:

CrowdStrike trades at a 24× ARR multiple - a giant outlier compared to peers growing at similar rates:

- HubSpot: 9×

- Elastic: 6×

- Confluent: 6×

- Zscaler: 15×

CrowdStrike is still one of the best companies in SaaS, full stop. But a business growing 20% with expanding CAC payback simply doesn’t look like a 24× multiple story. Something needs to change - or the multiple will.

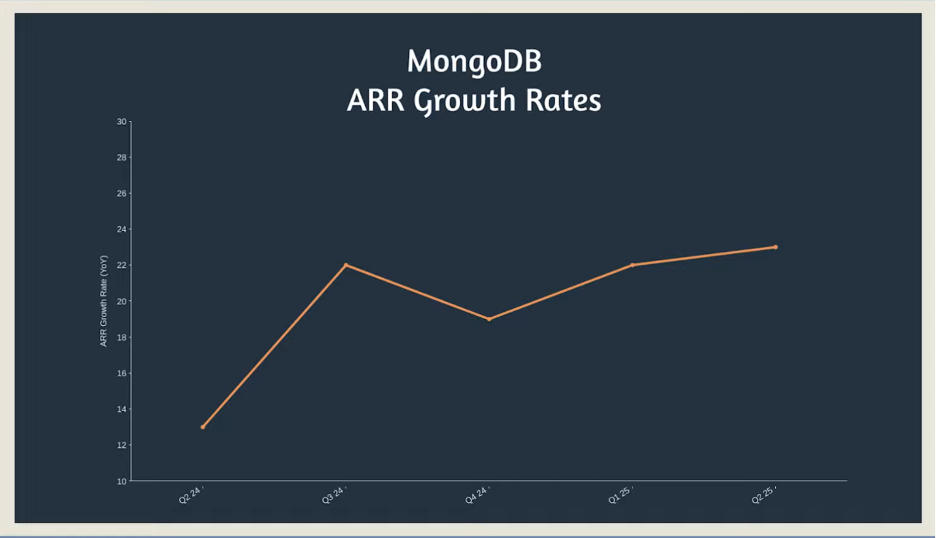

MongoDB: The Quietest Turnaround of the Quarter

MongoDB delivered arguably the cleanest quarter of the bunch - and the market noticed. The stock jumped 35% after earnings, adding $6.4B in market cap.

Why the enthusiasm?

Because everything is moving the right direction:

- ARR growth re-accelerated to 23% (vs 13% last year)

- CAC payback improved 33 → 23 months

- FCF margin flipped from –1% → +12%

- Operating margin improved –15% → –11%

MongoDB has quietly been executing a shift upmarket, and it’s working. They now have 2,564 customers paying more than $100K per year - up 17%.

In the last year they added $434M in net new ARR, with $164M of that coming in just the last quarter.

The market rewarded them with a ~10.5× ARR multiple.

Not cheap, but deserved.

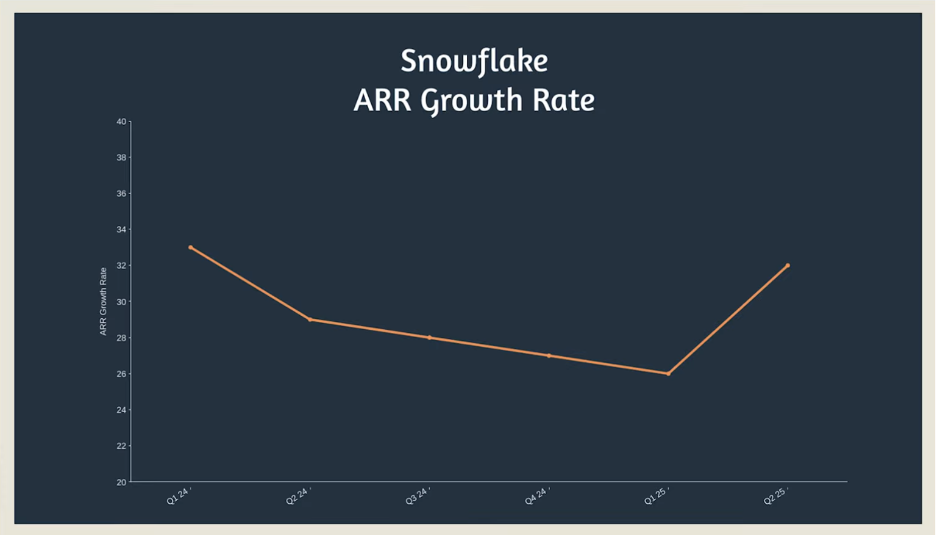

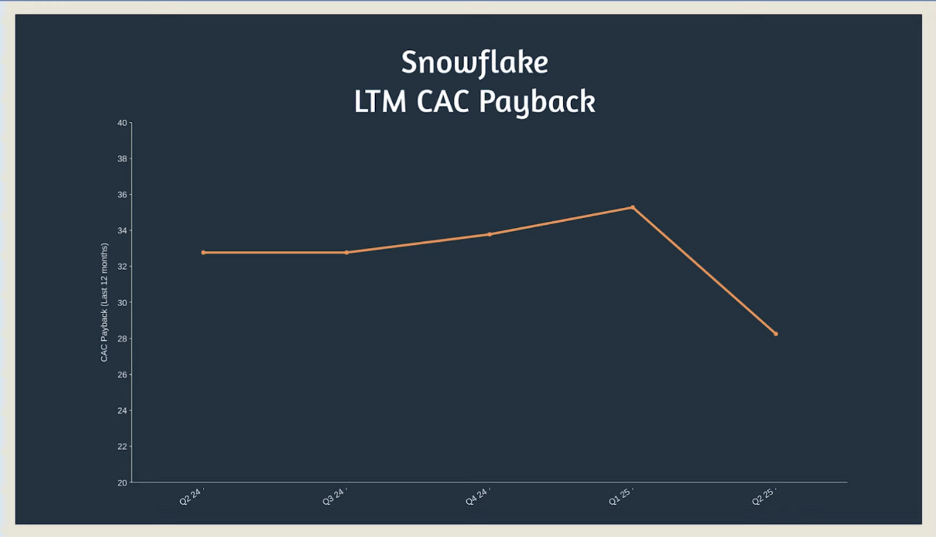

Snowflake: Growth Is Back - Profitability Is Not

Snowflake delivered something we haven’t seen much of in SaaS lately:

an honest-to-god re-acceleration in ARR growth.

After four straight quarters of slowing, ARR growth ticked up to 32%, the strongest since early 2024. They added $1B+ in net new ARR over the past year, putting them at $4.4B total.

And, like MongoDB, Snowflake improved CAC payback dramatically - to 27 months - on the back of stronger growth and more efficient GTM spend.

Their NRR remains one of the best in SaaS at 125%, even if it’s down from the 130–140% levels they saw in 2021–22.

But the flip side is glaring:

Snowflake is still one of the most inefficient operators at scale.

- Operating margin: –30%

- Operating loss: $340M

- FCF margin: just 5% (with improvements expected in 2025)

Rule of 40 came in at 37; Rule of X at 68.

Their multiple sits at 17× ARR - rich, but not unreasonable if the re-acceleration holds.

Benioff’s 20VC Interview: The AI Hangover Has Arrived

The second half of the episode featured Marc Benioff’s appearance on 20VC - and it was one of the more grounded, clear-eyed takes we’ve heard from a major SaaS CEO in a long time.

Benioff had three core insights worth paying attention to.

1. LLMs Are Impressive - But They’re Hitting Limits Faster Than Expected

Benioff’s view:

current LLMs are “finite algorithms trained on finite data,” and the industry is hitting diminishing returns faster than most people expected.

The launch of GPT-5 underscored that point:

instead of the leap everyone anticipated, we got incremental improvement.

Benioff’s message to customers?

AI is useful. It’s powerful. But it’s not magic - and the wildest predictions about agents replacing all human labor are “overblown.”

2. AI Is Already Transforming Two Functions: Support and SDR Work

Salesforce is living this internally.

Support

They reduced human support staff from 9,000 → 5,000 by deploying AI agents built on Agentforce.

In high-volume, high-repetition environments, LLMs shine.

Customers just want answers - they rarely care whether a human or machine delivers them.

Inbound SDR / Lead Qualification

Salesforce had 100M leads over 26 years that no human ever responded to.

Now they’re using AI SDRs to reach out, qualify, and route leads.

This is one of the most obvious near-term enterprise AI use cases - and Salesforce is betting big on it.

But Benioff emphasized: this isn’t about reducing headcount overall.

It’s about redeploying human talent into higher-value roles (AEs, SEs, revenue teams) and automating the repetitive work.

3. The Future of SaaS Interfaces Is Up for Debate

There’s a growing belief in the market that the future of SaaS looks like:

- one interface

- one agent

- connected to all your systems

- doing tasks across multiple apps

- without you ever logging into anything

Some call this “the database + agent” future - where traditional SaaS interfaces disappear and everything collapses into a chat-style workflow.

Benioff... didn’t buy it.

His response:

“If you think that, you’re really wrong. That’s crazy talk.”

But when pressed, he didn’t offer a compelling counterargument.

His position was essentially: we need apps and agents working together right now, and we’ll keep needing them for the next five to ten years.

It was more worldview than logic.

And it opens the door to the big question:

Are we heading toward a world where agents replace most front-end SaaS interfaces? Or do apps remain the primary way we work?

The Bottom Line

Q2 confirmed several truths about the SaaS market in 2025:

- Growth is harder than ever, especially above $1B ARR

- Efficiency is improving across the board - out of necessity

- A handful of companies (MongoDB, Snowflake) are bending the curve up again

- Premium multiples require either re-acceleration or flawless execution

- GenAI is powerful - but far from the sci-fi stories some people are selling

- And the future of SaaS interfaces is still genuinely up for debate

Thanks for reading - see you next week.

Meet with our founder

Want to meet to discuss what an outbound engine would look like in your business?