Every quarter, SaaS earnings season gives you a snapshot of where the market is heading.

But this quarter felt different.

Some companies are proving that efficiency at scale is possible.

Others are running out of room to hide.

And one company - Monday.com - is being punished for reasons that don’t match reality.

Let’s break it down.

Palo Alto Networks: Proof That Scale Doesn’t Have to Slow You Down

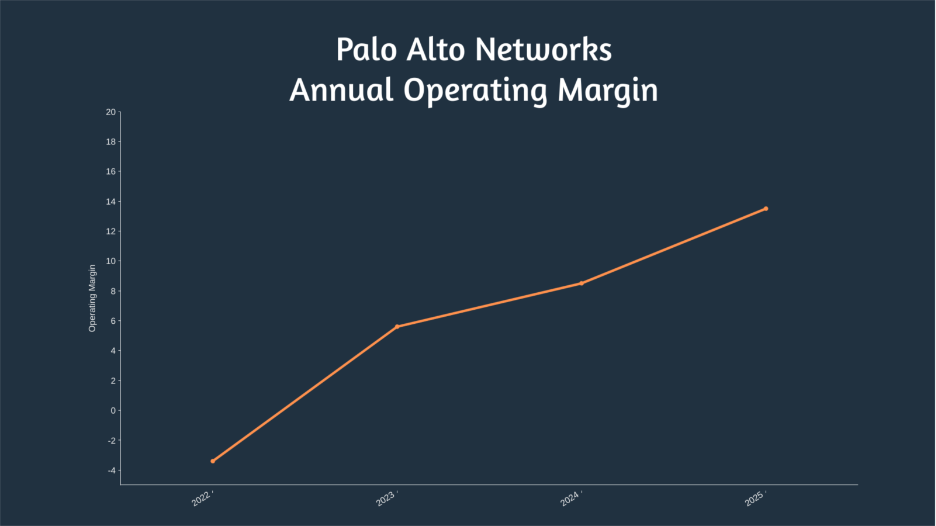

If you want to understand what elite SaaS execution looks like, start with Palo Alto Networks.

Q2 was another reminder that they’re operating in a different league:

- $500M+ in net new ARR in a single quarter

- $7.8B total ARR (plus half a billion in product revenue)

- 76% gross margins

- 120% NRR

- Operating margin now at 14%, up from –3.5% a few years ago

Most companies get slower and sloppier at scale.

Palo Alto just gets… better.

Even their CAC payback - 49 months - is completely fine when you’re adding nearly a billion dollars of recurring revenue every year.

At 15× ARR, the market knows exactly what it’s paying for: a machine.

Sprout Social: Growth Stalled, Efficiency Breaking

Then there’s Sprout Social - a company that once looked like a rising star in the social media management category.

Not anymore.

ARR growth has slowed to 13%, and the last few years tell the real story:

- 45% → 10% → low teens

- CAC payback now 75 months

- Free cash flow basically flat

- Rule of 40 at 17

This isn’t a company hitting temporary turbulence - it’s a company struggling to find its next gear.

The market is pricing Sprout at 2× ARR, which is basically the market saying:

“We’ll believe the turnaround when we see it.”

Fair.

SimilarWeb: Good Product, Tough Story

SimilarWeb joined our tracker this quarter, and it’s a fascinating business: lots of enterprise adoption, a valuable dataset, and a strong product.

But the financial picture is tougher.

ARR is $234M, growth is 17%, and efficiency metrics are going in the wrong direction:

- CAC payback up to 41 months

- Operating margin worsening from –2% → –10%

- Free cash flow margin cut in half

- R&D spend ballooning

Nothing is broken, but nothing is accelerating either - and in this market, “not accelerating” might as well be “standing still.”

At 2.6× ARR, they’re priced accordingly.

Monday.com: A Great Company Caught in a Bad Narrative

Now for the most interesting story of the episode: Monday.com.

The stock is down 40%+ over six months, and if you only followed Twitter analysts, you’d think Monday was getting eaten alive by AI tools.

But that’s not actually what happened.

What really caused the selloff? Two things:

1. Google’s AI answer box shaved off low-intent SMB traffic.

Not high-intent traffic.

Not demos.

Not pipelines.

Just the early-stage “What is project management?” type searches.

It’s a temporary top-of-funnel shift - not a structural threat.

2. Monday raised revenue guidance… but not “enough” for analysts.

Monday always raises second-half guidance.

This year, the raise was smaller because macro conditions are uneven and buyers are cautious.

That was enough for the market - already rotating hard into AI-native stories - to punish the stock.

The narrative snowballed, and suddenly Monday found itself priced like a middle-of-the-pack SaaS company.

Which is wild, because the fundamentals tell the opposite story.

The Numbers Say Monday Is One of the Best Operators in SaaS

Here’s what Monday actually delivered:

- $1.2B ARR, growing 26%

- 25% free cash flow margin

- 28-month CAC payback

- A market cap of $9.2B → only 7.6× ARR

That multiple puts Monday below peers that grow slower, generate less cash, or operate with worse efficiency.

Monday is:

- outperforming Procore

- outperforming HubSpot

- matching GitLab’s growth

- beating MongoDB on efficiency

Yet it trades at a discount to all of them.

That’s not a business problem.

That’s a market mood problem.

So Why Does This Matter?

Because moments like this create a divide:

- Companies like Palo Alto show what best-in-class looks like.

- Companies like Sprout and SimilarWeb show what happens when efficiency slips.

- And companies like Monday show how the market can misread short-term noise and undervalue long-term execution.

This quarter wasn’t just about earnings.

It was a snapshot of the SaaS landscape in 2025:

Efficiency is non-negotiable.

Narratives move faster than numbers.

And sometimes the market gets the story wrong.

Final Thought

If you follow SaaS operators closely, this was one of the more revealing quarters in years.

Not because the numbers were shocking - but because the reactions were.

Sometimes the market behaves like a voting machine.

Sometimes it behaves like a weighing machine.

Right now?

It’s doing a bit of both.

Meet with our founder

Want to meet to discuss what an outbound engine would look like in your business?